Sarina Shuqi Yang

July 2, 2025

Once hailed as a symbol of timeless elegance and the benchmark for luxury trench coats, Burberry is gradually fading from the dazzling spotlight of the fashion world.

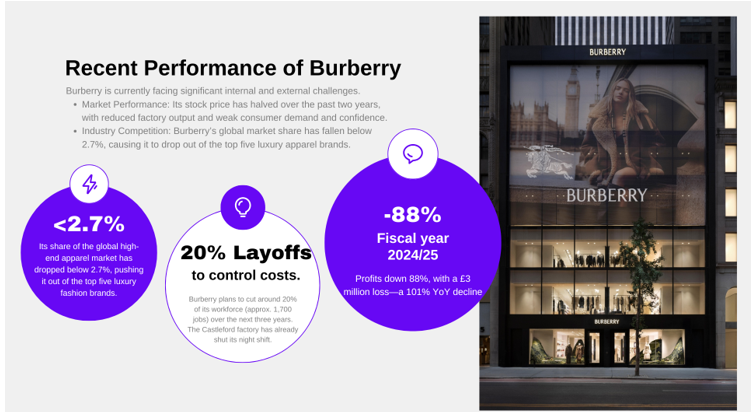

Sluggish Market Performance: Burberry’s market performance has been disappointing. In August 2024 and May 2025, its stock price hit decade-long lows, at one point dipping below £7 per share. Although there was a mild rebound thereafter, it has hovered around £10—well below the pandemic low of £14 in 2020, and a sharp decline from the £20 peak in 2023. In just two years, the stock has effectively been halved.

Beyond mere fluctuations in market capitalization, multiple indicators suggest Burberry is struggling to maintain growth:

Brand Dilution: Reckless Expansion and Misalignment with Customer Needs

Burberry’s aggressive expansion has resulted in a dilution of brand equity, steering the company away from core customer needs. Frequent discounting has further damaged its brand image. In recent years, Burberry’s performance in the Asia-Pacific region has exposed cracks in its luxury positioning. The brand has relied heavily on outlet stores to clear excess inventory, offering deep discounts on iconic trench coats, signature check scarves, and bags. This has led to declining traffic in flagship stores while outlet malls draw long lines.

According to HSBC, outlet stores now account for around 30% of Burberry’s sales and a staggering 50% of its net profit—far above the luxury industry average of just 5%. As a result, consumers are increasingly reluctant to pay full price at retail stores, undermining Burberry’s identity as a luxury brand.

In contrast, brands like Gucci and Hermès have upheld their exclusivity by tightly controlling distribution and supply. Burberry’s frequent promotions and clearance sales have led consumers to see it as more replaceable and less aspirational.

Losing High-Net-Worth Clients While Failing to Win Over Youth

Despite some success in attracting younger shoppers, Burberry’s core clientele remains the affluent, “old money” demographic who value craftsmanship, timeless design, and cultural heritage. While short-term sales have been boosted by price cuts, channel expansion, and product diversification, these moves have eroded brand prestige. Long-time customers lament that the brand no longer offers a distinctive luxury experience, weakening loyalty and repurchase intent.

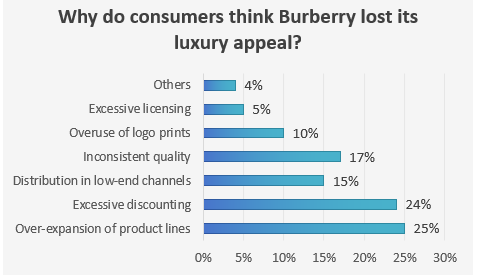

Focus group research among both high-net-worth individuals (35+) and younger consumers (18–35) reveals a concerning trend: 68% of affluent customers believe frequent discounting and product line expansion have made Burberry too mainstream, stripping it of its exclusivity.

One respondent put it bluntly: “When I see Burberry on sale, the whole experience feels cheap. Luxury should be unique.”

Consumers over 35 are especially sensitive to the weakening of the “old money” image, with one saying: “It once stood for prestige; now it feels too accessible, and has lost its former glory.”

Meanwhile, younger consumers, though more open to variety and accessible pricing, criticize the brand’s lack of a clear identity. Burberry’s attempt to appeal to both ends of the market has left it pleasing neither.

Brand Storytelling and Scarcity Are Key to a Turnaround

Recent consumer studies show that what truly resonates with consumers is not discounts, but compelling storytelling rooted in heritage and scarcity. Over 80% say they are more inclined to purchase after seeing campaigns focused on Burberry’s classic trench coats, British craftsmanship, and cultural legacy. Many admitted, “I wanted to buy it immediately after watching the storytelling ad.”

In contrast, price-driven promotions may attract short-term attention but fail to build lasting loyalty. The research is clear: telling a powerful brand story is essential to Burberry’s recovery and identity rebuild.

The Road Ahead: Balancing Prestige and Market Expansion

Moving forward, Burberry must strike a delicate balance between maintaining its high-end positioning and scaling its market reach.

At the crossroads of British tradition and global ambition, the question remains — where should Burberry’s transformation lead? Perhaps the brand’s most loyal supporters are those who still appreciate its refusal to follow fleeting trends.